Apr 1, 2026

Productive Debt: How Idle Capital Earns

Yield-bearing loan assets create a rate floor, so capital earns even when utilization is low.

DeFi lending markets have long treated idle capital as dead weight. When utilization falls, lending yields collapse, even when the underlying dollars could be earning somewhere else.

Lotus takes a different approach. By using a yield-bearing loan asset, Lotus gives deposited capital a built-in base rate even when utilization is low. The result is a more efficient market: more durable rates for lenders, tighter spreads for borrowers, and less dead capital.

More broadly, this points to a new design pattern for onchain credit: lending markets can be built around a yield-bearing base layer, not around idle stablecoins.

The Problem: Idle Capital Earns Nothing

Lending markets punish low utilization. The math is simple:

supplyRate = borrowRate × utilizationRate

At a 5% borrow rate and 50% utilization, suppliers earn 2.5%. Half the capital sits idle, earning nothing. This is true across all major lending protocols: the loan asset (typically USDC) simply stagnates.

Why should idle capital earn zero?

The Fix: Make Debt Productive

In Lotus markets, the loan asset is LotusUSD, a yield-bearing vault designed to keep idle lending capital productive.

Its reserve design is built to track a low-risk base yield while maintaining liquidity for instant borrowing and withdrawals. The Lotus app bundles USDC ↔ LotusUSD conversions into supply, withdraw, borrow, and repay transactions—users interact in USDC, but the underlying asset works harder.

This changes the fundamental economics. Instead of idle capital earning nothing, every dollar deposited earns the base yield from LotusUSD's reserves. The borrow rate decomposes into two components:

borrowRate = baseRate + creditSpread

The base rate is LotusUSD’s intrinsic yield—what the backing earns regardless of lending activity. The credit spread is what borrowers pay for the tranche's risk. Supply rates change accordingly:

supplyRate = baseRate + (creditSpread × utilizationRate)

Even at zero utilization, suppliers earn the base rate. That's productive debt.

The Math

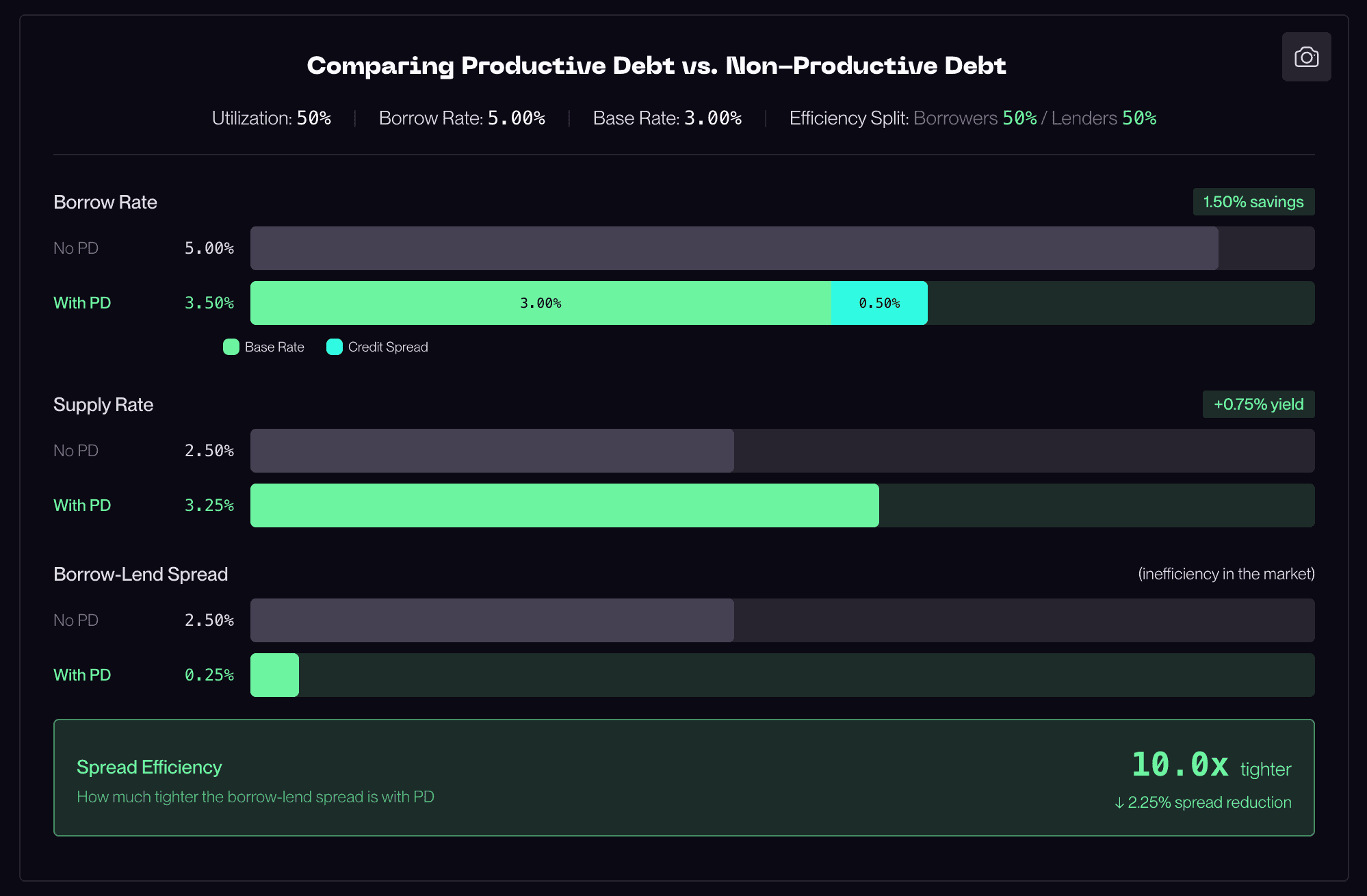

Take a traditional lending pool: 5% borrow rate, 50% utilization. Suppliers earn 2.5%.

Now consider a Lotus market with the same 5% borrow rate and 50% utilization, but decomposed into a 3% base rate and a 2% credit spread.

Model | Calculation | Supply Rate |

Traditional | 5% × 50% | 2.5% |

Productive Debt | 3% + (2% × 50%) | 4.0% |

The net spread, the gap between what borrowers pay and lenders earn, drops from 2.5% to 1%. That's a 1.5% efficiency gain. But who captures it?

The less obvious part: borrowers benefit too.

In a competitive market, that efficiency doesn't all flow to lenders. It gets split. The figure below shows a 50/50 distribution: borrowers pay 3.5% instead of 5% (1.5% savings), lenders earn 3.25% instead of 2.5% (0.75% higher yield). The net spread compresses from 2.5% to 0.25%—10x tighter.

Lower utilization amplifies the advantage. At 50% utilization, productive debt turns a mediocre market into an efficient one. At 30% utilization, it's the difference between a functional market and one that can't attract capital.

Try it for yourself. See how different utilization and money market returns affect rates across the ecosystem with our interactive docs.

Why Lotus Requires Productive Debt

Productive debt isn't a nice feature for Lotus markets. It's structurally required.

The Cascading Liquidity Problem

Lotus tranches share liquidity. When capital supplied to a junior tranche isn't borrowed at that risk level, it flows down to serve borrowers in more senior tranches. This prevents liquidity fragmentation—capital is always working.

But cascading liquidity creates a side effect: senior tranches exhibit lower utilization than they would in isolation. A senior tranche has its own direct supply, plus overflow from every junior tranche above it. More supply in the denominator means lower utilization, even if borrowing demand stays constant.

Without productive debt, that cascaded liquidity dilutes senior returns. Senior tranches would be structurally penalized for receiving overflow.

The Fix

With productive debt, low utilization in senior tranches is not a problem. Senior tranches have low credit spreads because they're the safest position in the market. In a traditional model, a 4% borrow rate at 30% utilization yields a 1.2% supply rate. On Lotus, senior lenders still earn the full base rate on 100% of their capital; the low utilization only affects the credit spread component, which is already small.

The result is a 3.3% yield instead of 1.2%.

Without productive debt, Lotus would face a choice:

Keep cascading liquidity, accept that senior tranches earn near-zero during normal conditions

Remove cascading liquidity, fragment the market into isolated pools

Neither works. The first makes senior tranches unattractive to any rational allocator. The second defeats the entire purpose of connected markets.

Productive debt makes cascading liquidity sustainable.

What You're Exposed To

Productive debt isn't magic yield. The base rate comes from real assets with real risks—they're just different risks than DeFi yield strategies.

Risk | Source | What It Means |

Issuer risk | USDC | Circle counterparty exposure |

Tokenization risk | Tokenized money market funds | Smart contract and custodial risk from tokenization partners |

Program dependency | Coinbase Prime | Part of LotusUSD’s yield depends on Coinbase Prime’s USDC rewards program, which is subject to eligibility, terms and rate changes. |

Rate variability | Fed policy | Base rate moves with short-term money market yields |

Liquidity timing | Reserve mix | Large redemptions during low utilization may face timing constraints |

USDC is already backed by short-term treasuries and cash equivalents. You're not taking on categorically new risk, you're transitioning from a non-yield-bearing wrapper to a yield-bearing one. The difference is you can see exactly what you're exposed to before you deposit.

If you want zero exposure to tokenized money market funds or USDC issuer risk, LotusUSD markets aren't for you. But you know that upfront. That's the point.

Stay in the loop: Follow on X | Join Telegram

Dive deeper: Explore our interactive docs

New to Lotus? Read the introduction