Mar 20, 2026

Connected by Design: How Lotus Works

How tranched markets, cascading supply, and productive debt work together to build better vaults.

This is the third in a series on how Lotus rethinks DeFi lending. For more context, start with the introduction and the problem.

Overview

Vaults are packaging. The product is the market structure they allocate into.

Most lending protocols force one risk setting on everyone in a market. Lotus does not. A Lotus market contains multiple risk-ordered tranches inside one shared market, so borrowers and lenders can choose different points on the same risk-return spectrum without splitting liquidity into separate pools. Three ideas make that work: a risk curve across ordered tranches, cascading supply that keeps liquidity connected, and productive debt that gives USD markets a base rate. Vault managers allocate into that structure; this piece explains the structure itself.

The result is not just more customization. It is a different market design. Risk is not hidden behind one protocol-wide compromise. It is exposed, ordered, and priced.

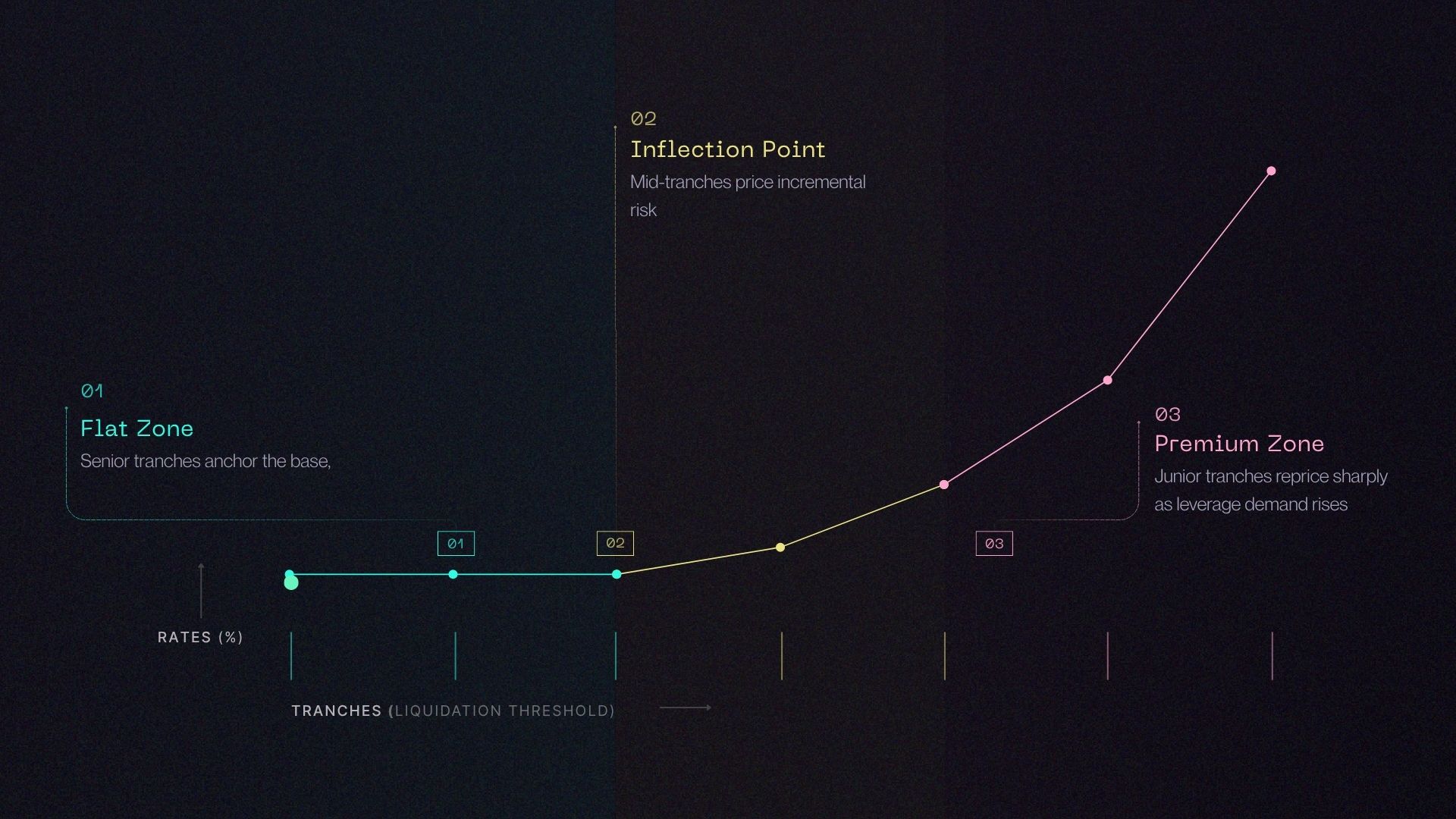

Markets and Tranches: The Risk Curve

A traditional lending market has one set of risk parameters for every participant. That works until borrowers and lenders want different tradeoffs. Borrowers usually want higher capital efficiency. Lenders usually want more liquidation buffer. One LLTV per market forces both sides into the same compromise.

Lotus turns that compromise into market structure. A market is a set of risk-ordered tranches that share a loan asset, interest rate model, and liquidation module. A tranche is one risk configuration inside that market, defined by its collateral, oracle, and LLTV. In current markets, tranches are ordered by LLTV: lower LLTV tranches are more senior, lower risk, and cheaper to borrow from; higher LLTV tranches are more junior, higher risk, and more expensive. Here, senior and junior describe risk appetite, not payment priority.

That ordering creates the risk curve. A conservative lender who wants BTC/USD exposure with more room before liquidation can supply to a senior tranche. A borrower who wants more leverage can borrow from a junior tranche and pay for it. They are in the same market, but they are not forced into the same terms.

Today, Lotus markets are LLTV-ordered. More broadly, the architecture can order tranches along other risk axes as well. The important point here is simpler: Lotus lets the market price risk directly across ordered tranches instead of prescribing it.

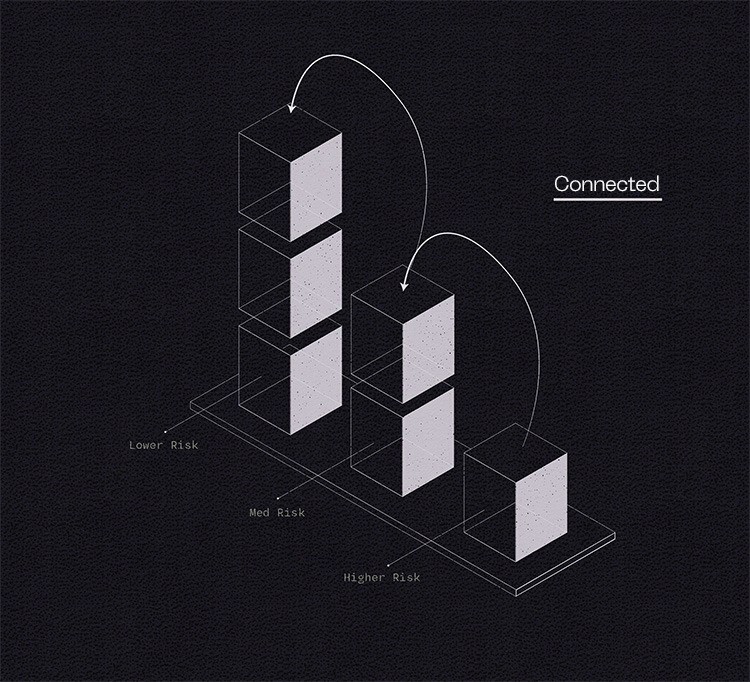

Cascading Supply: How Capital Stays Connected

Multiple risk tiers usually create a new problem: fragmented liquidity. If each risk level lives in its own isolated pool, some pools stay shallow even when nearby demand is strong. Rates disconnect. Capital sits idle in one place while borrowers pay up somewhere else.

Lotus solves that with cascading supply. Unused liquidity in junior tranches can support borrowers in more senior tranches. The flow is one-way: junior to senior, never the reverse. That matters because it keeps a lender from being exposed to more risk than the tranche they chose.

The result is a market that stays connected. A borrower in a senior tranche can access more liquidity than that tranche’s direct deposits. A junior lender can earn from demand at their own tranche and from more senior borrowing when local demand is lighter. A tranche can therefore show more borrowed than directly supplied, and capital does not sit idle just because activity is uneven across the stack.

That is the key design point. You can pick a risk tier without accepting a shallow market. Lotus keeps one market deep while still letting each participant choose where they sit on the curve.

Experiment with how different supply and borrow inputs affect performance across tranches →

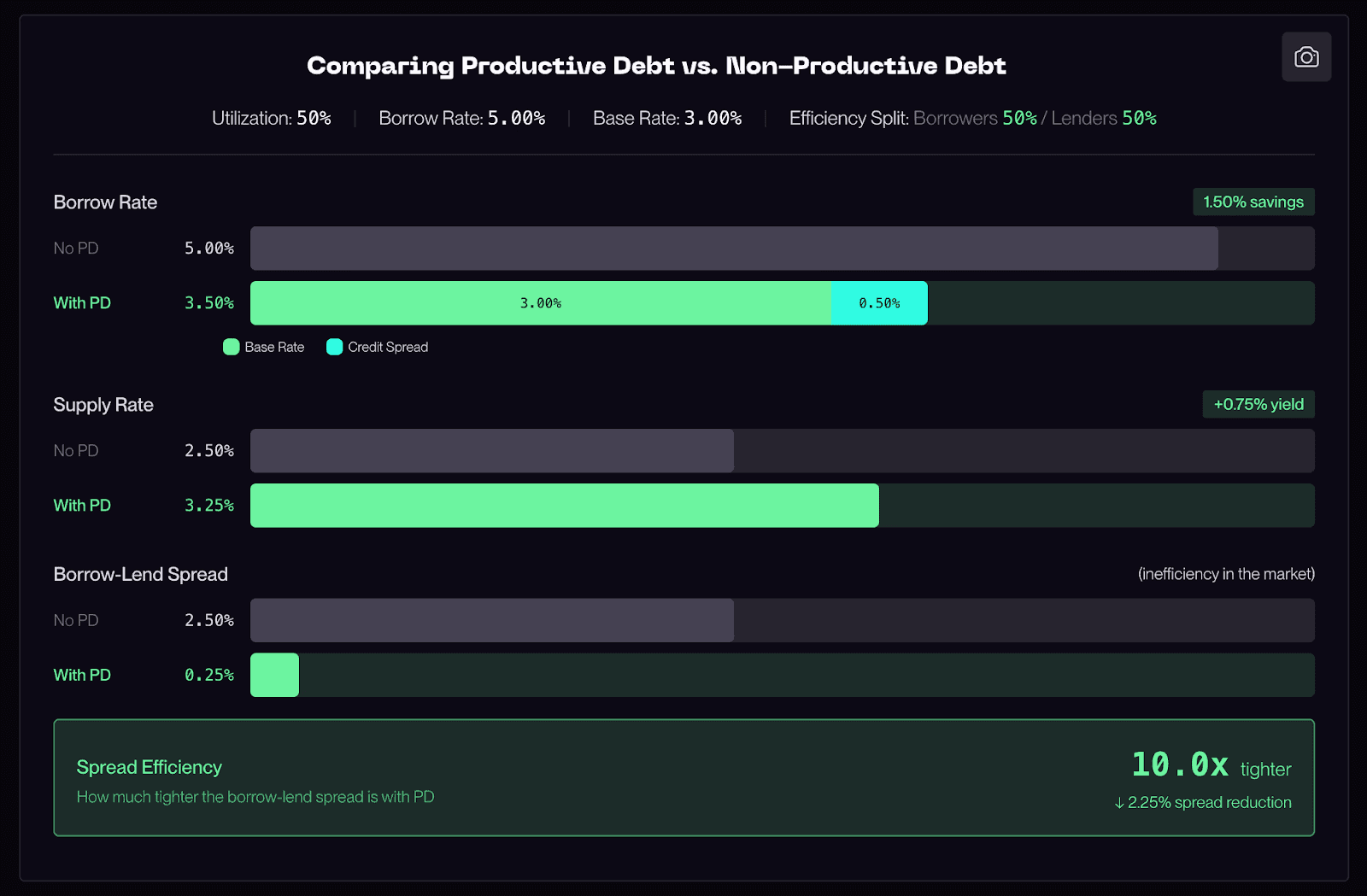

Rates and Productive Debt: How Pricing Works

Lotus still prices credit the way lending markets should: utilization drives rates. As borrowing demand rises and spare liquidity falls, borrow rates rise. As demand cools and liquidity returns, rates fall. In Lotus, that pricing happens across a tranche-based market, so rates adjust with demand while preserving the ordering of the risk curve.

That ordering matters. A riskier tranche should not become cheaper than a more senior tranche just because local demand is temporarily light. Lotus uses a market-level IRM so utilization can move rates while the curve itself stays economically coherent.

In USD markets, Lotus adds a productive base layer. LotusUSD is the yield-bearing vault at the base of the stack, backed by low risk tokenized money market funds. A portion remains in idle USDC to support instantaneous borrows and withdrawals, while the remainder earns a base yield from those underlying assets. The most senior tranche is effectively base-rate credit; more junior tranches add spread on top. That is what creates productive debt.

Productive debt means the borrow rate has two parts:

Borrow Rate = Base Rate + Credit Spread

The base rate comes from LotusUSD. The credit spread is the market-specific premium for borrowing at a given tranche. Because the base rate exists underneath the market, lenders keep a floor even when utilization is low, and the IRM only has to price the credit component.

That changes the economics in two useful ways. First, idle capital is still productive instead of sitting as dead reserve (particularly useful with new market launches where suppliers lead borrowers). Second, the spread between what borrowers pay and what lenders earn compresses, because part of the return is structural rather than purely dependent on borrowing demand. It also makes rates less jumpy. Utilization still matters, but it is moving the credit spread rather than the entire return stack.

Users do not handle LotusUSD directly. The protocol routes USDC into and out of LotusUSD in the same transaction, so users still interact in USDC while the market gets the benefit of productive backing underneath.

Adjust utilization and watch the spread compress between borrowers and lenders →

Liquidations and Bad Debt: What Happens When Things Go Wrong

A position stays healthy only while it remains inside its tranche’s limits. If LTV rises above LLTV, the position becomes eligible for liquidation. A liquidator repays debt, receives collateral according to the liquidation module, and the protocol uses that process to convert collateral back into loan repayment.

If liquidation fully covers the loan, the system works as intended and lenders are made whole. If it does not, the shortfall becomes bad debt.

Lotus keeps debt and collateral accounting aligned with the tranche structure, so losses stay with the risk that produced them. Bad debt is not socialized across the entire market. Interest and loss allocation follow the tranche structure, which means the suppliers who backed the defaulted exposure absorb the shortfall according to the same underlying exposure that earned the interest in the first place.

In practice, that means a junior loss stays where junior risk was taken. If a high-LLTV position fails under stress, the loss sits with the tranche exposure that funded it rather than leaking across the whole market. You know what has to fail before you take a loss, and you are not underwriting tranches you did not choose.

See how bad debt is absorbed across tranches →

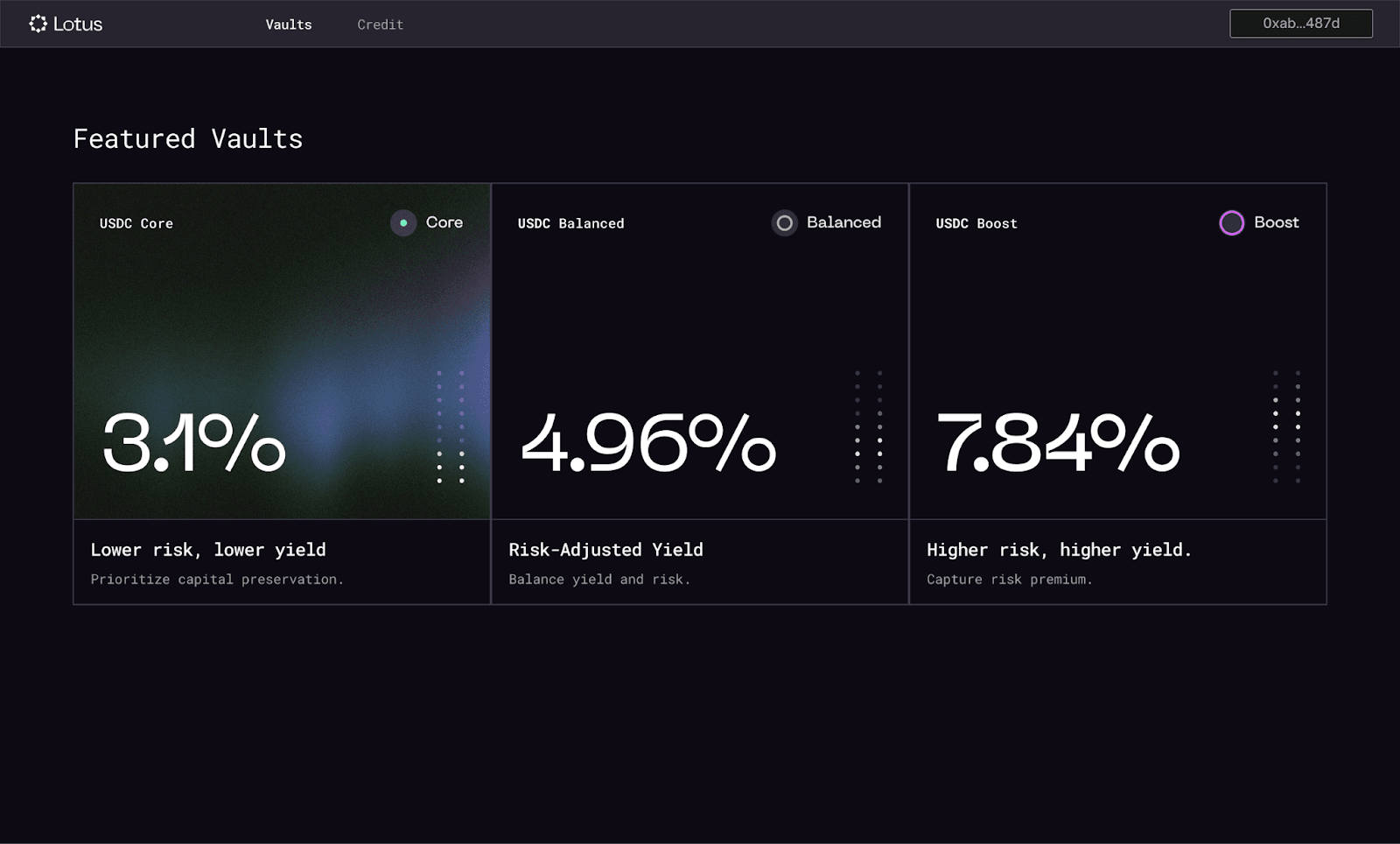

Vaults: How Most People Will Actually Use This

Most lenders will not want to pick tranches manually. They will use vaults.

A Lotus vault lets you deposit one asset and receive shares while a professional manager allocates across markets and tranches according to a mandate. Conservative vaults can stay concentrated in senior tranches. More aggressive vaults can move further down the risk curve. The point is not to hide the mechanism, but to package it into something most users can actually use.

That makes manager quality legible instead of hand-wavy. The curator defines the strategy and risk boundaries. The allocator moves capital within those limits. The sentinel can de-risk in emergencies. Fees are explicit. Independent risk ratings by Credora can also help users verify that a vault’s actual exposures match its stated mandate. You are delegating tranche selection, not surrendering visibility into what the vault owns.

That is where the architecture becomes a product surface. Vaults are wrappers over ordered tranches, connected liquidity, and productive debt. You choose the mandate; the manager executes it; the underlying exposures remain visible.

Compare vault strategies and see how allocation shifts across the risk curve →

Why This Architecture

Every lending architecture makes tradeoffs. Lotus makes three explicit ones.

First, it does not force one market-wide risk setting on everyone. It lets lenders and borrowers meet across an ordered curve instead.

Second, it does not split every risk tier into isolated pools. It connects them through cascading supply so depth is preserved.

Third, in USD markets, it does not rely on borrower demand alone to create lender yield. Productive debt gives the market a base layer of return before credit spread is added on top.

Those choices are what make Lotus vaults possible. The vault is the wrapper. The market structure is the engine.

Closing

This is the market structure Lotus vaults allocate into. Ordered tranches let the market price risk directly. Cascading supply keeps that market deep. Productive debt gives USD credit a base rate.

If you want the full mechanics, explore documentation or interactive research . If you want to evaluate the product, this is the system you are evaluating.

Follow our progress toward launch here.