Mar 26, 2026

Choose Your Tranche: Borrow on Your Terms

Borrow against BTC and ETH with higher leverage, tighter spreads, and more stable rates.

This week, we published Connected by Design: How Lotus Works, the full architecture behind Lotus's connected tranche market. That same architecture creates structural benefits for borrowers.

At a Glance

Lotus expands optionality for borrowers without fragmenting liquidity. In a typical onchain lending market, one set of risk parameters applies to all participants. Lotus markets let borrowers choose where they sit on the risk curve and set their terms accordingly.

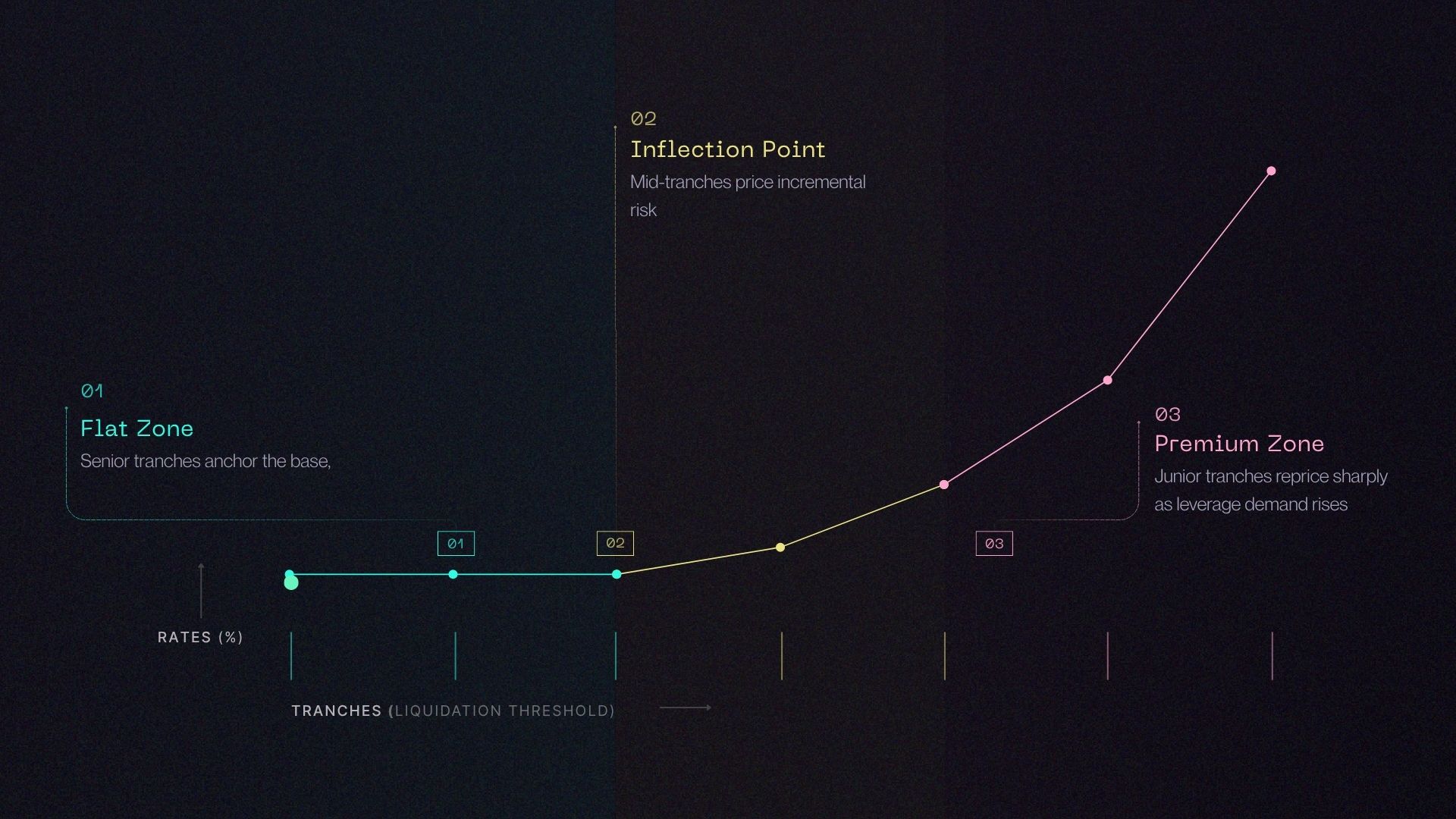

BTC-USD and ETH-USD markets with tranches ordered by LLTV (80% to 95%)

Higher LLTVs are junior tranches; lower LLTVs are senior tranches

Up to 20x leverage at 95% LLTV vs. 4-7x in existing protocols

Choose capital efficiency at a higher rate, or stable low rates on conservative loans

Refinance between tranches as conditions change – no need to unwind positions

Why Borrowing Against BTC and ETH Still Feels Broken

Onchain borrowing is permissionless, transparent, and always-on. But, for professional borrowers, it still comes with three recurring pain points.

Limited Leverage

Because traditional lending protocols only have one set of risk parameters for the entire market, the loan terms are set conservatively to avoid bad debt at all costs. If any risk was transferred from the borrower to the lender, it would cause conservative, low-LTV borrowers to subsidize higher-LTV ones. With Lotus’s approach, each borrower and lender can independently choose where they sit on the risk curve enabling participants on both sides of the market to price different loan terms. Ultimately, this means that a borrower with a high opportunity cost of capital can take out a higher leverage loan which is funded by lenders willing to absorb the higher level of risk.

Instead of needing perpetual futures or offchain prime broker lines, traders can get high capital efficiency financing onchain with Lotus.

Inefficiency

Unborrowed capital in existing lending protocols sits idle, which increases the net spread – the difference between borrow and supply rates. As a result, DeFi lending today has a major structural inefficiency that causes lenders to earn less while borrowers pay more.

Borrowers in Lotus benefit from lower rates as a result of productive debt. In USD-denominated markets, borrowers receive loan proceeds in USDC, but debt is tracked in units of a vault token, which deploys USDC to tokenized money market funds.

Borrowers pay the spread on top of the vault’s rate. This efficiency gain compresses the net spread, allowing lenders to earn the same yield while borrowers pay a lower total interest rate.

Volatile Rates

Existing lending protocols rely on utilization to price interest rates for the entire pool. This means that conservative borrowers are subject to rate spikes even when the risk of their loan is still extremely low. Volatile rates cause funding costs to jump abruptly, destroying trade economics and forcing active position management.

With Lotus, interest rates are not reliant on utilization as the only input and each tranche rate is priced as one adaptive curve. The result is that interest rates remain low and stable for conservative borrowers accessing senior tranches.

Because of limited leverage and volatile rates, many institutions don’t structure their products and trades using DeFi lending markets, opting instead for the benefits of other funding rails as described below.

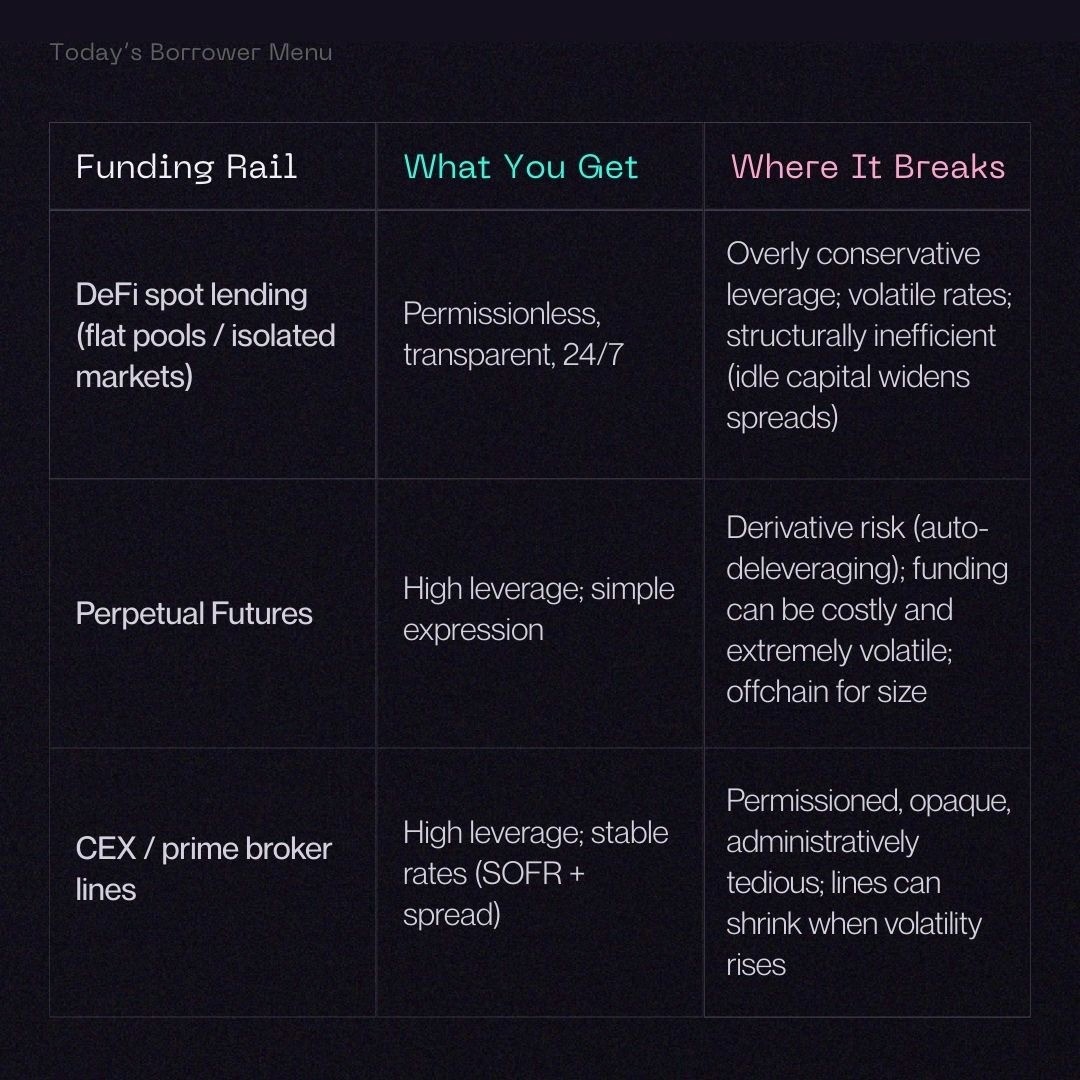

The Borrower’s Menu Today

What Lotus Changes

Lotus introduces BTC-USD and ETH-USD funding markets with a connected ladder of risk-tiered tranches that share information and liquidity. Rather than fragmenting supply across isolated pools, Lotus creates a single market where different loan terms, such as LLTV, can be priced along a continuous risk curve.

This provides borrowers flexibility across the risk curve. For example:

High‑leverage junior tranches for borrowers who value capital efficiency (e.g. basis/carry, cross‑venue arbitrage, tactical leverage)

Stable low-interest senior tranches for borrowers who primarily care about predictable funding for inventory, longer‑horizon strategies and minimizing trade admin.

How Rates are Priced and Which Tranche to Choose

At a high-level, interest rates are set across the risk curve to provide an equal all-in cost for borrowers at an adaptive return on equity. Individual borrowers will have different opportunity costs of capital, and so it is not only the interest rate that matters to the borrower. The all-in cost is the interest rate on the borrowed amount plus the opportunity cost on the amount not borrowed against the collateral. The interest rates across the risk curve are set to equalize the all-in cost at a given opportunity cost.

If an individual borrower has a higher opportunity cost than the market’s internal opportunity cost, they will prefer to borrow from the most junior tranches as that would give them the lowest all-in cost. Alternatively, borrowers with a lower opportunity cost will prefer to borrow from more senior tranches as this minimizes their all-in cost. The competing forces allow Lotus markets to adapt to the borrower preferences. At the same time, lenders – and their risk appetite – determine which tranches they are willing to supply to. The market prices all of this information and creates an adaptive risk curve.

As a borrower, you’re able to choose where you sit on the risk curve. If you are able to deploy a highly profitable strategy using borrowed funds, your internal cost of capital will increase making it more profitable to use a more junior tranche. If that external strategy’s returns decrease, you can simply refinance back to a more senior tranche.

See how these tradeoffs work in practice with the interactive borrowing calculator.

Running basis, carry, or inventory strategies on BTC/ETH? Lotus is allocating early borrower capacity ahead of mainnet. Contact jordan@lotuslabs.net.